Can I Keep My Motorcycle When the Insurance Company Totals It?

Yes. You can keep a totaled motorcycle if the insurance company declares it a total loss. The motorcycle is your property, and it is always your choice whether to keep it or not.

The insurance company will pay you for the total value of your motorcycle plus tax, less the salvage value. You can purchase the vehicle back for scrap value with a salvage title.

Many of our clients are attached to their motorcycles and want to keep them at any cost. We have had clients who know how to repair or rebuild motorcycles and clients who built a custom motorcycle and wanted to rebuild it.

Who Owns a Totaled Motorcycle After Insurance Pays for the Motorcycle?

Since the insurance company will pay you for your totaled motorcycle, the insurance company will own the motorcycle after they pay you for it.

The insurance company will pay you for your totaled motorcycle less the salvage value. A salvage company will pay you the salvage value. You must give the motorcycle title to the insurance or salvage company.

How to Buy Back Your Totaled Motorcycle

If you want to keep your motorcycle, you must buy it back for the salvage value from the insurance company (see below for how much it can cost).

Just tell the insurance company that you want to keep your totaled motorcycle. The insurance company will pay you for the damage to your motorcycle, less the salvage value. You will not be paid the salvage value. You will keep your motorcycle and get a salvage title.

![]()

Get New York Motorcycle Accident Lawyers Rob Plevy, Esq. and Phil Franckel, Esq. at the 1-800-HURT-911® Personal Injury Dream Team™ on your side and become a member of our family!

“I endorse these guys 100% they handled my motorcycle accident very well! And they are genuine human beings.”

—Frank Sundancer Perugi

Please take a look at some of our:

We created the popular motorcycle awareness campaign you know and have seen!

No Win — No Fee — No Expenses — Guaranteed!

Think you were at fault or other lawyers said you don’t have a case, please call us!

At HURT911® you can speak, text, or email Rob Plevy, Esq. and Phil Franckel, Esq. whenever you need throughout your case and afterward, days/nights/weekends.

Call days/nights/weekends for a free consultation with no obligation.

Call right now! 1-800-HURT-911 | 1-800-487-8911

![]()

![]()

Motorcycle Attorney Phil Franckel talks about how motorcycle accidents are different

Philip L. Franckel, Esq. is the author of all articles and content on this website, one of the Personal Injury Dream Team™ Founding Partners at 1-800-HURT-911® New York, well-known for representing motorcyclists. He has a 10 Avvo rating; Avvo Client’s Choice with all 5-star reviews; Avvo Top Contributor; and is a former Member of the Board of Directors of the New York State Trial Lawyers Association. Mr. Franckel created the motorcycle awareness campaign BE AWARE MOTORCYCLES ARE EVERYWHERE®.

Founding Partner Rob Plevy, Esq.

New York Motorcycle Accident Lawyer and Founding Partner Rob Plevy, Esq.

Robert Plevy, Esq. is a motorcycle accident lawyer and one of the Personal Injury Dream Team™ Founding Partners at 1-800-HURT-911® New York. Robert began his legal career in 1993 as an Assistant Corporation Counsel defending The City of New York against personal injury lawsuits.

Get the HURT911® Personal Injury Dream Team™ on your side!

Call Attorneys Rob Plevy & Phil Franckel days/nights/weekends for a free consultation

1-800-HURT-911

1-800-487-8911

![]()

How Much Will it Cost to Buy Back a Totaled Motorcycle?

The cost to buy back a totaled motorcycle is the salvage value, usually only a few hundred dollars. We usually see motorcycle salvage values ranging from $250 to $750.

But you don’t have actually to pay that money. You will just receive less money from the insurance company. The insurance company will pay you for the damage to your motorcycle, less the salvage value.

Example:

$7,500 motorcycle value before it was totaled

$500 motorcycle salvage value

$7,500 amount you receive if you do not keep your motorcycle

$7,000 amount you receive if you keep your motorcycle with a salvage title

If you’re in New York, read what you need to know about Salvage Branding and the New York Salvage Vehicle Examination Program.

If you want to repair your motorcycle, always use a qualified motorcycle repair shop unless you’re highly experienced.

Totaled Motorcycle Financed With a Bank Loan

If you financed your motorcycle by buying it with a bank loan, the bank will have a lien on your title.

The insurance company will pay off the bank loan and give you any excess amount. If the insurance company does not pay enough to pay off the bank loan, you must pay the difference to the bank.

You can keep a totaled motorcycle with a salvage title when a bank financed the motorcycle. You just have to pay the salvage value to your insurance company.

Why Will the Insurance Company Keep a Totaled Motorcycle?

When you have collision or comprehensive (fire and theft) coverage, and you make a claim for damage to your motorcycle, the insurance company will pay you for the damage.

If the insurance company determines that the damage will cost too much to repair, the insurance company will total the motorcycle, take possession of it, and sell it for salvage value.

When Is a Motorcycle Totaled?

In New York, a motorcycle will be totaled if the cost to repair is 75% or more of the motorcycle’s value.

Motorcycles are totaled by the insurance company in the vast majority of our motorcycle accident cases. We have even seen motorcycles totaled when there was almost no visible damage.

Often, the insurance company won’t even send an appraiser to the repair shop to inspect your motorcycle. They will call the shop and ask the shop to email photos of the motorcycle.

Our cases always involve an injury from a motorcycle accident. But just like a motorcycle can be totaled with little to no visible damage, a rider can be seriously injured even when the motorcycle has little to no visible damage. Even if you only had a minor injury from a motorcycle accident, call us!

Why Do Insurance Companies Total Motorcycles With Little Damage?

Because most motorcycles are worth considerably less than cars, the cost of repairing a motorcycle is proportionately more than repairing a car. Therefore, motorcycles are totaled more often than cars.

Often, the fork and/or frame is bent, or there is a crack in the motor or other parts, and the cost to repair the motorcycle is just too much compared to the value of the motorcycle.

The damage to the motorcycle in this photo doesn’t look too bad, but if you look closely at the photo, you can see cracks on the fairing and damage to the gas tank and handlebar. Not so visible was that the fork was bent. The motorcycle was totaled.

The insurance company totaled the motorcycle because of this damage

Is it a Good Idea to Keep a Totaled Motorcycle?

Rarely. Unless you have an antique or highly collectible motorcycle with considerable value, keeping a totaled motorcycle won’t make sense.

Examples of Clients Who Wanted to Keep a Totaled Motorcycle

We had a client who was unhappy when the insurance company offered him $8,000 for his Harley Davidson with a Screaming Eagle package. He wanted to keep the motorcycle, but we checked with Harley Davidson and were told that his Screaming Eagle package was a dealer add-on and not collectible. We then got the insurance company to pay $13,000, so he decided to take the money.

We had another client, Manny, who built his own custom motorcycle that looked like a “Mad Max” motorcycle.

Manny wanted to purchase his totaled motorcycle with a salvage title and rebuild it because he spent hundreds of hours building it, but the insurance company only offered him $12,000. We paid for an estimate to build an identical custom motorcycle and got the insurance company to pay $28,000, which was much more than our client wanted.

Continue reading below this section

![]()

Injured? Call 1-800-HURT-911® Founding Partner Rob Plevy right now for your free consultation!

Injured? Call 1-800-HURT-911® Founding Partner Rob Plevy right now for your free consultation!

Rob will call you back within minutes!

1-800-487-8911

![]()

![]()

No Win — No Fees

— No Expenses

— GUARANTEED! ™

You know our Motorcycle Awareness Campaign!

Listen to Phil, Rob & Donna, who bought a brand new house after we settled her case! What will you do with your money?

![]()

Is It Worth It to Keep a Totaled Motorcycle?

Following are the cons or downsides you must consider if you decide to keep your totaled motorcycle after an accident.

Salvage Title

You will get a salvage title if you keep your motorcycle after the insurance company totals it.

A salvage title is stamped SALVAGE to be obvious to a buyer. A salvage title will significantly reduce the value of your motorcycle and affect your insurance.

Read about salvage titles at Edmunds.

Resale Value

A totaled motorcycle will have a lower resale value.

You wouldn’t want to buy a motorcycle with a salvage title for the same amount as a motorcycle with an unbranded title. So, don’t expect to sell your motorcycle for full value if the title is branded as salvage.

A salvage title will significantly reduce the value of your motorcycle because it tells prospective buyers that the motorcycle was severely damaged. In New York, it says that the damage was at least 75% of the motorcycle’s value before the accident.

Insurance With a Salvage Title

If you have a salvage title, your insurance premium will likely be higher. You may also have difficulty finding an insurance company to insure a motorcycle with a salvage title.

If you find an insurance company to insure a motorcycle with a salvage title, your insurer will probably only cover liability.

If the insurer only offers liability for a salvage motorcycle, you will not have collision coverage if the motorcycle is damaged, and you will not have comprehensive, which includes fire and theft coverage.

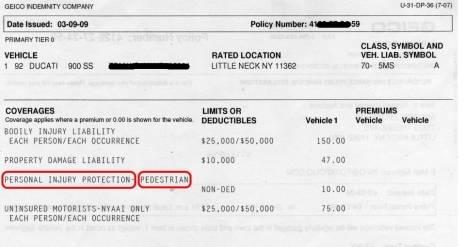

See our Ultimate Motorcycle Insurance Guide to learn about the different types of motorcycle insurance coverage.

Salvage Cost

You will have to pay the salvage value. But paying the salvage cost is not really a downside to buying a totaled motorcycle.

When an insurance company pays you for the loss of your motorcycle, you’re being paid for 100% of the motorcycle’s value in the condition it was in before being damaged.

Because you’re being paid 100% of the motorcycle’s value, the insurance company is entitled to take the motorcycle and sell it to recoup some of its money.

Paying the insurance company the salvage value for your totaled motorcycle is just paying the insurance company back for what they paid you. And you’re only buying it from the insurance company for what it’s worth.

The insurance company will deduct a few hundred dollars from the money they pay you for your totaled motorcycle. Most totaled motorcycles have a salvage value of $500-800. Whatever the salvage value is, your insurance company will deduct that from the money they pay you.

If you want to buy your totaled motorcycle, you will not be paid the salvage value. Therefore, your cost to buy your totaled motorcycle is the amount of the salvage value.

Open Recalls

If your motorcycle has a salvage title and your motorcycle has open recalls, the dealer may deny repairing the recall. This also applies to cars.

What Should I Do if I Don’t Have Collision Coverage and the Car’s Insurance Won’t Pay Enough for My Motorcycle?

If you were injured in a motorcycle accident in New York, we will represent you for free for your motorcycle damage claim. It may take longer to get the money for your motorcycle than if you had collision coverage, but we won’t charge you a legal fee, and we have been very successful getting full value from the other car’s insurance for our clients’ motorcycles, so you’re likely to get all your money back.

Note: We do not represent motorcyclists for motorcycle collision damage unless you were injured.

See why we highly recommend collision coverage for motorcycles. If you don’t have collision coverage on your motorcycle, you’ll probably find that the other driver’s insurance won’t pay you 100% of your motorcycle’s value.

![]()

Philip L. Franckel, Esq. personally authored this page and all articles on NYMotorcycleAttorneys.com.

Philip L. Franckel, Esq. personally authored this page and all articles on NYMotorcycleAttorneys.com.

You may have met Phil Franckel and Rob Plevy at motorcycle events. Phil and Rob created the motorcycle awareness campaign BE AWARE MOTORCYCLES ARE EVERYWHERE®. They are Founding Partners of 1-800-HURT-911® New York, well-known in New York for representing motorcyclists. Phil is an Avvo Top Motorcycle Attorney with a 10 Avvo rating, Avvo Motorcycle Client’s Choice award with all 5-star reviews, Avvo Top Motorcycle Accident Contributor, and a former Member of the Board of Directors of the New York State Trial Lawyers Association.

![]()

Get New York Motorcycle Accident Lawyers Rob Plevy, Esq. and Phil Franckel, Esq. at the 1-800-HURT-911® Personal Injury Dream Team™ on your side and become a member of our family!

“I endorse these guys 100% they handled my motorcycle accident very well! And they are genuine human beings.”

—Frank Sundancer Perugi

Please take a look at some of our:

We created the popular motorcycle awareness campaign you know and have seen!

No Win — No Fee — No Expenses — Guaranteed!

Think you were at fault or other lawyers said you don’t have a case, please call us!

At HURT911® you can speak, text, or email Rob Plevy, Esq. and Phil Franckel, Esq. whenever you need throughout your case and afterward, days/nights/weekends.

Call days/nights/weekends for a free consultation with no obligation.

Call right now! 1-800-HURT-911 | 1-800-487-8911

![]()

![]()

Motorcycle Attorney Phil Franckel talks about how motorcycle accidents are different

Philip L. Franckel, Esq. is the author of all articles and content on this website, one of the Personal Injury Dream Team™ Founding Partners at 1-800-HURT-911® New York, well-known for representing motorcyclists. He has a 10 Avvo rating; Avvo Client’s Choice with all 5-star reviews; Avvo Top Contributor; and is a former Member of the Board of Directors of the New York State Trial Lawyers Association. Mr. Franckel created the motorcycle awareness campaign BE AWARE MOTORCYCLES ARE EVERYWHERE®.

Founding Partner Rob Plevy, Esq.

New York Motorcycle Accident Lawyer and Founding Partner Rob Plevy, Esq.

Robert Plevy, Esq. is a motorcycle accident lawyer and one of the Personal Injury Dream Team™ Founding Partners at 1-800-HURT-911® New York. Robert began his legal career in 1993 as an Assistant Corporation Counsel defending The City of New York against personal injury lawsuits.

Get the HURT911® Personal Injury Dream Team™ on your side!

Call Attorneys Rob Plevy & Phil Franckel days/nights/weekends for a free consultation

1-800-HURT-911

1-800-487-8911

![]()

There is a legal principle called “Negligent Entrustment,” which can allow the motorcyclist to be compensated for his injuries from his mother’s motorcycle insurance.

There is a legal principle called “Negligent Entrustment,” which can allow the motorcyclist to be compensated for his injuries from his mother’s motorcycle insurance.