What is Underinsured Coverage? What You Need To Know, How Much You Need & Where To Get It

Uninsured & Underinsured Coverage Protects You from Cagers!

To easily get back to this page, just go to CagerProtection.com

Vote in the Underinsured poll!

How to Protect Yourself Against Cagers

What’s a Cager?

A word used by some motorcyclists, often in a derogatory manner, to describe drivers of cars who sit in a cage (car body) and don’t pay attention or see what’s around them. Cagers don’t see motorcycles.

How much underinsured coverage do you really need when you get hit by this cager?

Hint: This driver is about to hit you, you’ll probably get an injury worth $500,000, and he only has $25,000 coverage!

Find out how we’ll give you money to help protect you!

What’s Underinsured Coverage?

It’s the most important coverage on your motorcycle insurance policy because it pays you!

Uninsured coverage will pay YOU money when you are injured because of the negligence of someone who has no insurance or who left the scene of a hit-and-run accident.

Underinsured coverage will pay YOU an additional amount above the other car’s insurance coverage when they have less liability insurance coverage than your liability insurance limit.

Uninsured and underinsured coverage will not pay money to someone injured in the car that hit your motorcycle. This coverage only protects you and a passenger on your motorcycle.

Uninsured and underinsured coverage is sold by insurance companies in a package of the same amounts, so if you have $300,000 for one, you have $300,000 for the other.

Example: You have $300,000/$500,000 liability with $300,000/$500,000 underinsured coverage. If your ankle is broken when hit by a car with a $25,000/$50,000 insurance policy, the car has $275,000 less liability insurance than your liability insurance. Therefore, you can collect $25,000 from the car that injured you, and your motorcycle insurance company will pay you up to an additional $275,000 for a total of $300,000.

Even a torn meniscus (knee injury) can be worth a lot of money because it will cause serious problems as you get older. We obtained a $465,000 verdict for a motorcyclist who had a torn meniscus. See what a knee injury and other injuries can be worth.

Funny Video Explaining Underinsured Coverage

Insurance Agents in New York Must Offer to Sell Matching Uninsured/Underinsured Coverage

In 2003, Attorney Phil Franckel, as a Member of the Board of Directors of the New York State Trial Lawyers Association (NYSTLA), lobbied NYS Sen. James L. Seward, Republican Chair of the Insurance Committee. After lobbying issues for NYSTLA, Phil Franckel suggested his idea for two new laws to Sen. Seward and was later reprimanded by the Association for proposing his own ideas.

One law would help get uninsured cars off the road, and the other law would require insurance agents to offer matching uninsured and underinsured coverage.

Phil Franckel suggested insurance companies and agents be required to sell uninsured and underinsured limits in the same amount as (or matching) the amount of liability insurance a person is purchasing.

After several years it was sponsored by Senator Seward in bill S.7787 and later passed both houses.

NY Governor Andrew Cuomo initially vetoed the law, but in December 2019, Gov. Cuomo finally signed the law that changed how SUM (Supplemental Uninsured/Underinsured) coverage is sold. The law finally went into effect in June 2019.

Since motorcycle accidents usually cause serious injuries, this law substantially benefits motorcyclists.

How the Old Law Worked

Under the old uninsured/underinsured law, if a car with $25,000 insurance coverage or no insurance coverage ran a red light and hit your motorcycle, causing a serious injury, you would receive only $25,000 instead of as much as $500,000 or more.

This is because insurance companies were only required to sell $25,000 uninsured coverage and no underinsured coverage. Motorcyclists rarely had more than $25,000 uninsured coverage or any underinsured coverage.

Most people would ask for minimum insurance or full coverage. Minimum insurance coverage does not include underinsured coverage, and there’s no such thing as full coverage.

Even if you asked for full coverage, you probably wouldn’t be told about underinsured coverage. You had to know about underinsured coverage and request it.

Insurance agents rarely offered it, and since most people don’t know what it is, most drivers of cars and motorcyclists didn’t have it.

What the New Law Does

Now, when you ask for $100,000/$300,000 liability coverage, the insurance company is required to offer you $100,000/$300,000 uninsured and underinsured coverage unless you don’t want it.

If you purchase $50,000/$100,000 liability coverage, you’ll be quoted for $50,000/$100,000 uninsured and underinsured coverage.

If you purchase $25,000 liability coverage, you still won’t have underinsured coverage and won’t even be told about it because it’s not possible to buy underinsured coverage when you have only $25,000 liability coverage.

We recommend purchasing at least $250,000 liability, uninsured, and underinsured coverage for a motorcycle because there’s a high probability that you can have an injury that will keep you out of work for months.

The cost of increasing uninsured and underinsured coverage is very little and vitally important, especially to motorcyclists, because of the severe injuries often sustained in motorcycle accidents.

We recommend calling an independent motorcycle insurance agent to make sure you get the best advice and the right coverage for your motorcycle.

How to Find Out How Much Underinsured Coverage You Have Now

Most motorcyclists have only $25,000 uninsured coverage with $0 underinsured coverage!

Look for your motorcycle insurance policy DECLARATIONS PAGE. This is the page that shows a list of your coverage limits and how much you are being charged.

You may see uninsured and underinsured coverage listed on your motorcycle insurance policy as:

- Uninsured/Underinsured

- Supplementary Uninsured/Underinsured

- Supplementary UM

- SUM

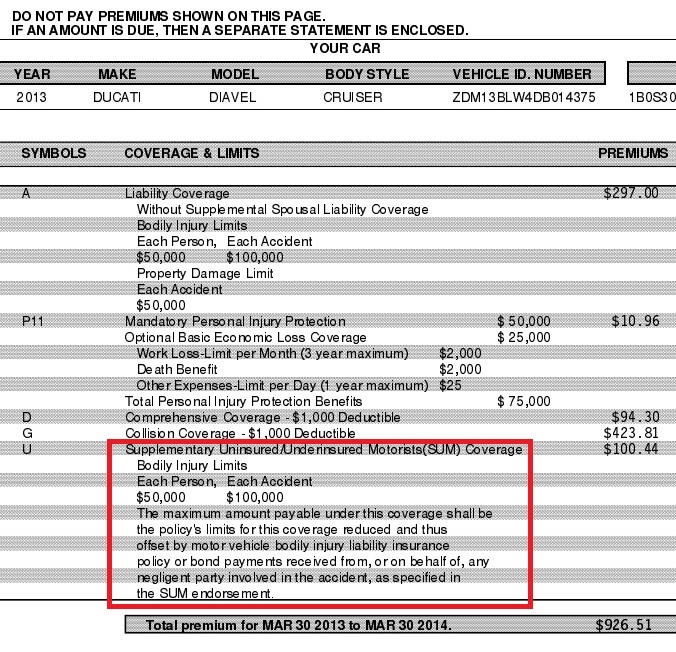

Example showing how Supplementary Uninsured/Underinsured Motorists Coverage is listed on a motorcycle insurance policy (will look similar on different policies). This example shows the motorcyclist has $50,000/$100,000, which will pay the motorcyclist up to $50,000 and up to $50,000 for a passenger and no more!

(click the image to see it larger)

Benefits of Underinsured Coverage

More money — Of course, the most important benefit is that you can get hundreds of thousands more money when you really need it — after you’re injured in a motorcycle accident. You will probably not be able to work for a few months. You will need money to pay your living expenses and medical treatment.

Speed up your case — A very important side benefit to having a high underinsured limit is that it can substantially speed up your case, getting money to you much faster, often in just months instead of 2-5 years. When your injuries keep you out of work, you need money quickly, not years later. If you don’t have health insurance to pay your medical bills, you’re going to need a lot of money very quickly.

When you have underinsured coverage higher than the at-fault car’s insurance, the car’s insurance will usually pay the entire policy quickly. This is because the defense insurance company knows we cannot get the additional money from your underinsured coverage without the at-fault car’s insurance paying the entire policy. They know if they don’t pay, we must go to trial with the car’s insurance company, and they really don’t want that.

Once the car’s insurance company offers to pay its insurance policy, the underinsured claim against your insurance company can be decided by arbitration within months instead of a lawsuit that can take years. Additionally, an arbitration usually costs less than $1,500, while trial expenses can cost as much as $15,000-$35,000.

Health insurance — If you have health insurance through a large company, you may have an ERISA health plan. New York State prohibits health plans from getting their money back from your case, but ERISA health plans can because they are regulated by federal law. They can’t take all your money, but some of it will have to go back to your ERISA health plan. Getting underinsured coverage will allow you to keep more money for yourself.

Do I Need Underinsured Coverage?

Yes. No motorcyclist should ever have less than $100,000, but many injuries from motorcycle accidents are worth more than $500,000 to as much as millions. We obtained a $465,000 jury verdict for a motorcyclist who struck the side of a car making a left turn, and he suffered a knee injury with a torn meniscus and arthroscopic surgery. A broken ankle can be worth $1 million. The loss of a leg can be worth $9 million.

We recommend a minimum of $2500,000 in underinsured coverage, but more is better! There are four insurance companies listed below that sell $500,000 coverage and two which sell $300,000. Please get quotes, and you’ll see it’s not expensive.

If you want or need to protect yourself when you are injured by a cager who has little or no insurance, you need underinsured coverage. Don’t complain about getting only $16,666 (after a one-third legal fee) when your ankle is broken because of a driver who has only $25,000 insurance.

Think insurance is a waste? If you waste your money on underinsured coverage because you’re never injured, it will be the best thing you ever wasted money on!

Let us prove the driver was at fault — You need to buy underinsured coverage to protect yourself from cagers!

How to Determine How Much Underinsured Coverage You Need

Injuries in most motorcycle accidents will keep you out of work for 4-12 months.

- Determine how much money you need to pay your bills if you are unable to work for 4-12 months. (mortgage/rent, utilities, TV, phones, car payments, insurance, gas, food, etc.

- Add 50,000-$100,000 for hospital and medical bills if you don’t have health insurance. If you do, add enough to cover deductibles and co-payments plus the cost of treatment, therapy, home care, and medications not covered by health insurance.

- Add how much more money you want for your pain and suffering if you are injured.

- Add 50% to the total, which adds enough to pay the 1/3 legal fee.

- The total amount of 1-4 is the amount of underinsured coverage you need to purchase.

Example Showing the Amount of Underinsured Coverage You Need

- You earn $75,000 per year with a net income of $48,750 after taxes.

- You have health insurance – add $15,000 for non-covered therapy, co-payments, and other expenses.

- You don’t want any additional money for your pain and suffering.

- To get the $63,750 you need (after legal fees), you have to buy $100,000 coverage.

To insure yourself for the minimum amount you need

$48,750 (lost income) + $15,000* (medical bills) + 50% (1/3 legal fee) = $95,625 (the amount you need). (Your future lost wages and future medical bills may be much more.)

Purchase at least $100,000 underinsured coverage since underinsured coverage is sold in amounts of $50,000; $100,000; $250,000 $300,000 or $500,000.

To insure yourself for the minimum amount you would like, including pain & suffering

$48,750 (lost income) + $50,000* (medical bills) + $100,000 (amount you want for your pain) + 50% (1/3 legal fee) = $298,750.

Purchase $300,000 or $500,000 underinsured coverage.

*Your medical bills could be much higher. While usually between $35,000 to $100,000 in motorcycle accidents, we have seen medical bills as high as $1 million.

Uninsured/Underinsured Calculator

— find out how much underinsured coverage you need.

The Underinsured Motorist Coverage calculator tool is free and easy to fill out in less than a minute. It will show you the minimum amount of underinsured coverage you need and the amount you should have on your motorcycle insurance and car insurance policy.

How Much Underinsured Coverage Can I Buy?

You can buy as much uninsured and underinsured coverage as you want up to your liability coverage limit. For instance, if you have $100,000/$300,000 liability, you cannot buy more than $100,000/$300,000 uninsured and underinsured coverage.

$100,000/$300,000 uninsured and underinsured coverage protects one person up to $100,000 and all people in a car or on a motorcycle up to $300,000. Since only one person is usually on a motorcycle, you can only get $100,000 when you have $100,000/$300,000 uninsured and underinsured coverage.

Most insurance companies have a maximum amount of uninsured and underinsured coverage they will sell. For instance, State Farm will sell you as much as $1,000,000 uninsured and underinsured coverage if you buy $1,000,000 liability. State Farm will sell not sell more than $1,000,000 in uninsured and underinsured coverage. But Chubb will sell you as much as you want.

New York State only requires you to have a minimum of $25,000 in Uninsured Coverage. You are not required to have Underinsured Coverage.

If you ride in other states, you should know that some states have low auto insurance requirements, such as $10,000, and some states don’t even require cars to have insurance. Underinsured/Uninsured coverage on your New York motorcycle insurance policy will protect you in all states.

In New York, underinsured coverage is sold together with uninsured coverage unless you have minimum coverage.

The amounts of Underinsured/Uninsured coverage that can be purchased to protect a motorcyclist, depending upon the insurance company, are:

- $25,000 Uninsured/$0 Underinsured (if you have minimum coverage)

- $50,000 Underinsured/Uninsured (totally inadequate for all motorcyclists)

- $100,000 Underinsured/Uninsured (inadequate for all motorcyclists)

- $250,000 Underinsured/Uninsured (the minimum amount you should consider purchasing)

- $300,000 Underinsured/Uninsured

- $500,000 Underinsured/Uninsured

- more than $500,000 Underinsured/Uninsured

What are split limits, and why they are not important to motorcyclists

Split limits look like $100,000/$300,000. This means your insurance company will pay no more than $100,000 to each person who is injured and no more than $300,000 to everyone injured in the accident.

Don’t forget that underinsured coverage pays money for you and your passengers. This money is not paid to someone injured in the car that hit you.

Since you won’t have more than two people on your motorcycle, if you have $100,000/$300,000 underinsured coverage, your insurance company will not be able to pay more than $200,000 in underinsured coverage payments, even though you have $300,000 total coverage. The motorcyclist can be paid $100,000, and the passenger can be paid $100,000.

If you ride alone and you have $100,000/$300,000 underinsured coverage, your insurance company will not pay you more than $100,000. If you ride alone, always look at the first figure if you have a split-limit insurance policy.

If you have a single-limit insurance policy with $300,000 single-limit underinsured coverage, the insurance company can pay you up to $300,000 for your injury and will not pay more than $300,000 for both you and your passenger.

Which Insurance Companies Sell the Most Underinsured Coverage?

Uninsured and underinsured coverage is sold either as a single limit (ex. $300,000 total for both motorcycle operator and passenger) or a split limit (ex. $100,000/$300,000). The lower number in the split limit is the maximum amount per person. If you don’t have a passenger riding on the back of your motorcycle, the amount you’re interested in is the lower amount.

I called 11 insurance companies that sell motorcycle insurance in New York and asked how much underinsured coverage they sell in NY (Note: you must purchase liability coverage in the same or a higher amount as your underinsured coverage. Make sure your underinsured coverage is as high as your liability coverage).

The coverage limits below show the amount that insures a motorcyclist without a passenger (if you have $100,000/$300,000, you really only have $100,000, and your passenger has $100,000.

I recommend that you call an independent insurance broker because when you buy directly from an insurance company, the “agent” is only a salesperson and will not give you advice.

List of insurance companies with the maximum amount of underinsured insurance coverage they sell in New York to cover YOU, the motorcycle operator, is as follows:

-

-

- Chubb – as much as you want – Find an agent

- State Farm – $1,000,000

- Liberty Mutual – $500,000 – Find an agent

- Foremost – $500,000 (sells for Farmers agents & 21st Century) – Get a quote

- Nationwide – $500,000 – Find an agent (enter your zip code)

- Progressive – $300,000

- GEICO – $300,000

- Allstate – $250,000

- Esurance – $250,000

- Dairyland – $250,000

- Farmers – $250,000

- MetLife – $250,000

- Markel – $250,000

- Amica currently sells through Progressive but will soon sell directly in NY

- The Hartford does not sell motorcycle insurance in New York

- Travelers do not sell motorcycle insurance in New York

- Kemper does not sell motorcycle insurance

-

Our recommendation is to purchase at least $500,000 but no less than $250,000. Specialized Insurance & Rossi Insurance sells motorcycle insurance and understands the importance of underinsured coverage for motorcyclists.

Review your coverage every time you renew your policy every spring or when you put your motorcycle back on the road because we have seen insurance companies reduce coverage back to the minimum after putting a motorcycle back on the road.

How Much Does Underinsured Coverage Cost?

With motorcycle insurance policies, underinsured coverage is far more important than liability coverage, but you have to increase your liability to increase underinsured coverage because you can’t buy a higher underinsured coverage amount than your liability coverage amount.

If you already have higher liability insurance limits, increasing your underinsured coverage will cost less. If you have minimum liability insurance limits, you will have to increase your liability limits so you can purchase underinsured coverage. However, increasing your liability limit on a motorcycle policy is not expensive and well worth the small cost to protect yourself with substantial underinsured coverage.

High underinsured coverage on a motorcycle can cost a few hundred dollars per year, but approximately 1/2 of our cases involve an injury worth $500,000 or more. For instance, we got a verdict of $465,000 for a knee injury with a torn meniscus.

You may be able to get a discount on your motorcycle insurance by taking a motorcycle school class, and we’ll pay you to take the class!

Video – Why You Shouldn’t Buy Full Coverage Insurance!

Motorcycle Insurance Guide

For information about other types of coverage on your motorcycle insurance policy, see our Motorcycle Insurance Guide with information about:

- Liability coverage

- Property damage liability

- The 3 types of collision and comprehensive coverage

- Additional Accessory Coverage

- What if you had an accident and didn’t have collision coverage

- Medical coverage and no-fault

Poll Question

Too much info? If you have any questions about your insurance coverage, call Phil Franckel 7 days/nights to discuss it for free (we don’t sell insurance, but we’ll give you free advice).

If you’re involved in a motorcycle accident, even if another lawyer doesn’t think you have a case, call us immediately for a free consultation. We care about motorcyclists!

![]()

Philip L. Franckel, Esq. personally authored this page and all articles on NYMotorcycleAttorneys.com.

Philip L. Franckel, Esq. personally authored this page and all articles on NYMotorcycleAttorneys.com.

You may have met Phil Franckel and Rob Plevy at motorcycle events. Phil and Rob created the motorcycle awareness campaign BE AWARE MOTORCYCLES ARE EVERYWHERE®. They are Founding Partners of 1-800-HURT-911® New York, well-known in New York for representing motorcyclists. Phil is an Avvo Top Motorcycle Attorney with a 10 Avvo rating, Avvo Motorcycle Client’s Choice award with all 5-star reviews, Avvo Top Motorcycle Accident Contributor, and a former Member of the Board of Directors of the New York State Trial Lawyers Association.

![]()

Get New York Motorcycle Accident Lawyers Rob Plevy, Esq. and Phil Franckel, Esq. at the 1-800-HURT-911® Personal Injury Dream Team™ on your side and become a member of our family!

“I endorse these guys 100% they handled my motorcycle accident very well! And they are genuine human beings.”

—Frank Sundancer Perugi

Please take a look at some of our:

We created the popular motorcycle awareness campaign you know and have seen!

No Win — No Fee — No Expenses — Guaranteed!

Think you were at fault or other lawyers said you don’t have a case, please call us!

At HURT911® you can speak, text, or email Rob Plevy, Esq. and Phil Franckel, Esq. whenever you need throughout your case and afterward, days/nights/weekends.

Call days/nights/weekends for a free consultation with no obligation.

Call right now! 1-800-HURT-911 | 1-800-487-8911

![]()

![]()

Motorcycle Attorney Phil Franckel talks about how motorcycle accidents are different

Philip L. Franckel, Esq. is the author of all articles and content on this website, one of the Personal Injury Dream Team™ Founding Partners at 1-800-HURT-911® New York, well-known for representing motorcyclists. He has a 10 Avvo rating; Avvo Client’s Choice with all 5-star reviews; Avvo Top Contributor; and is a former Member of the Board of Directors of the New York State Trial Lawyers Association. Mr. Franckel created the motorcycle awareness campaign BE AWARE MOTORCYCLES ARE EVERYWHERE®.

Founding Partner Rob Plevy, Esq.

New York Motorcycle Accident Lawyer and Founding Partner Rob Plevy, Esq.

Robert Plevy, Esq. is a motorcycle accident lawyer and one of the Personal Injury Dream Team™ Founding Partners at 1-800-HURT-911® New York. Robert began his legal career in 1993 as an Assistant Corporation Counsel defending The City of New York against personal injury lawsuits.

Get the HURT911® Personal Injury Dream Team™ on your side!

Call Attorneys Rob Plevy & Phil Franckel days/nights/weekends for a free consultation

1-800-HURT-911

1-800-487-8911

![]()